How-to: Find Out How Your Credit Is Doing

Table of Contents

![]()

A common misconception is that there’s no way of knowing whether your loan application will be approved or not beforehand. If your application is rejected, you are often left in the dark as to what the problem was with your creditability as a borrower.

Besides that, every time you are rejected for a loan, your credit health will take a hit because other financial institutions will be able to see that your previous application has been rejected. Just one rejection is enough for the following lender to see it as a red flag and reject you again – it seems to be a vicious cycle for someone with questionable credit health.

The thing is, you can actually find out how likely you’ll be approved for a loan beforehand by checking your credit reports. This lets you find out what’s bad when it comes to your credit and how to fix them before applying to avoid that circle of rejection.

You can do so by accessing your CTOS report to check if there are any red flags in the report that may impact your future credit applications. Here’s how you can finally take some of the unknowns from credit application, and maybe kiss rejection goodbye:

What is CTOS?

CTOS is a registered Credit Reporting Agency under the ambit of the Credit Reporting Agencies Act 2010. CTOS collates and provides individuals with their credit reports that detail their credit history for the past 24 months, legal proceedings, company ownership and directorship, and even testimonies from companies that they have business dealings with.

CTOS works both ways – you can check your personal report to ensure you are financially healthy, while companies (including financial institutions) can check your report to ensure you are credit-worthy for any loan or credit card applications. The information on your credit history will help banks evaluate your loan application and decide if you credible enough to be given a loan.

Before applying for any loan, you can evaluate your credit profile via CTOS to ensure your credit records are clear and free from any doubts so you get the best possible chance of getting an approval from the bank.

How to get your FREE MyCTOS report online?

MyCTOS report is your personal credit report by CTOS. The best thing about this report is, you can get it for FREE, and without leaving your seat.

1. Registration of account

To get the report online, you need to create an account on CTOS website. You can do so by just providing your identity card number (IC No.), email address and specify your language preference (English, Malay and Chinese).

You will then be required to fill up on some details about you or your company.

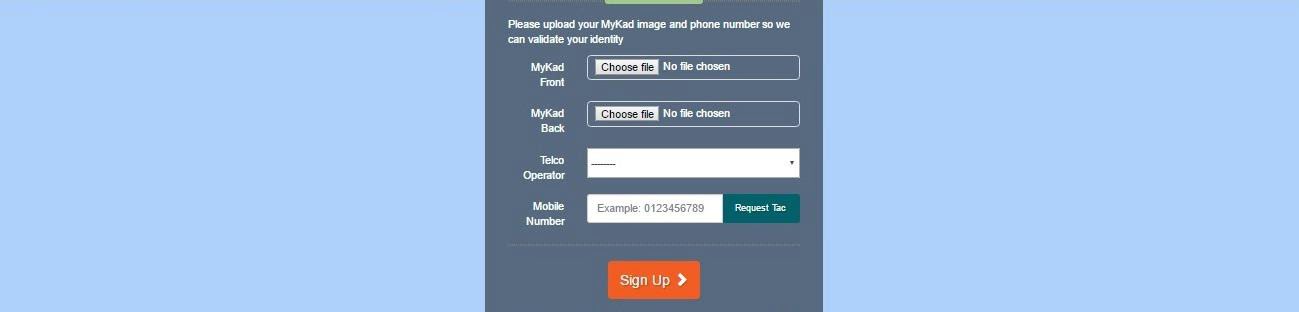

Then, attach the images (front and back) of your MyKad to verify your details, and fill in your mobile number.

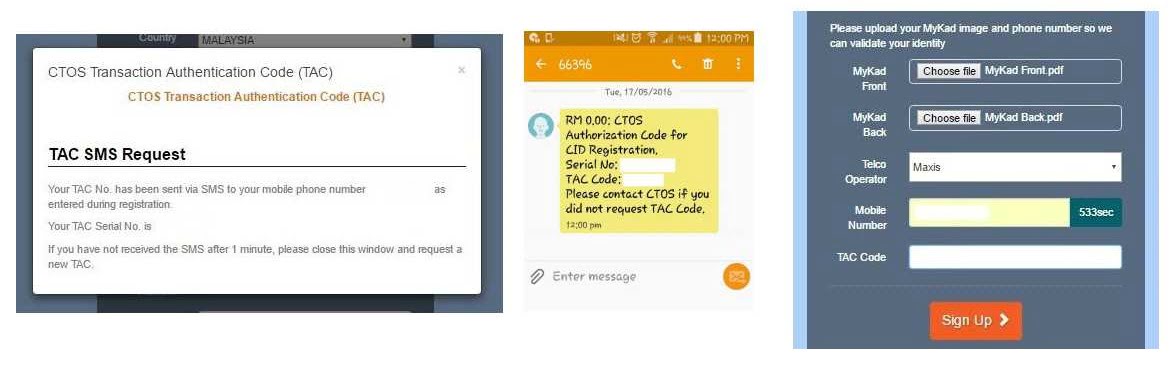

It is extremely important to provide the correct mobile number as a TAC verification code will be sent to your mobile to complete the registration process.

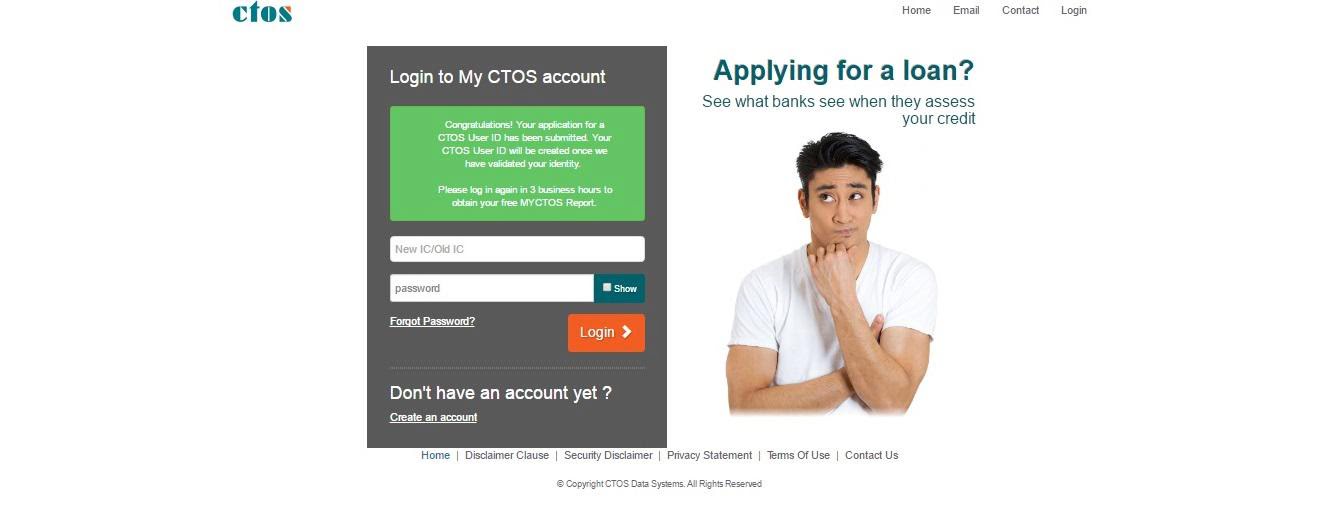

Upon submission, you will be sent a confirmation email where you will be notified that your registration is pending verification.

Typically, verification is done on the same day, and you will receive another email to inform you that your account has been verified, and registration is complete.

Once you’ve received your TAC code, key it in to complete the registration process.

2. Activation of CTOS ID

CTOS will require 3 working hours to verify your details and provide you with a valid User ID that you need to access your CTOS report.

You will receive an email from CTOS on your User ID details via the email address that you had provided earlier.

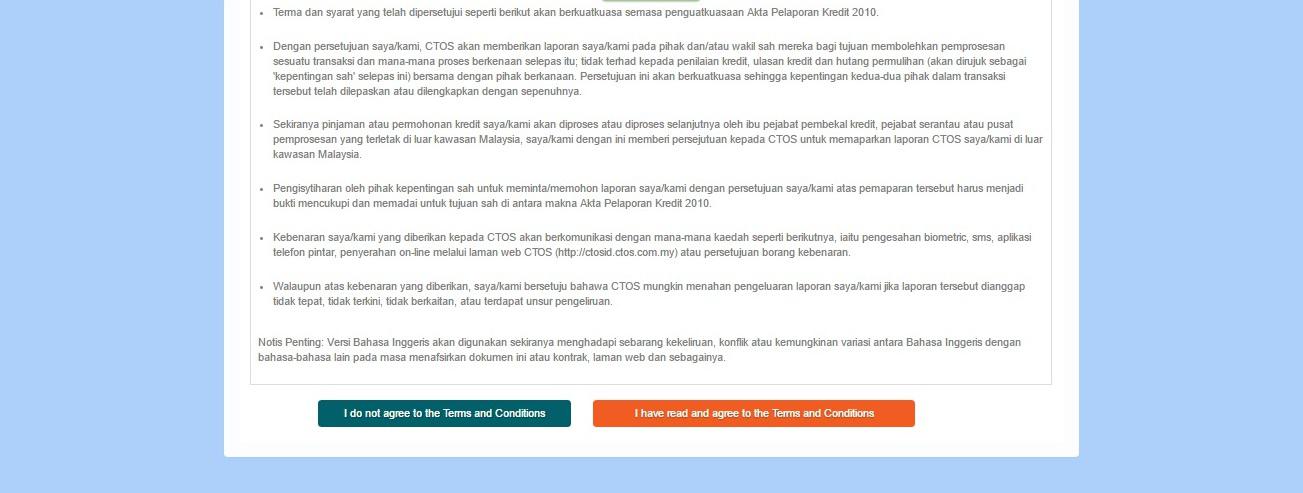

To complete the registration process, login with your user ID and your password, and proceed to accept the terms and conditions.

Choose a security question to ensure your account is well secured and cannot be logged easily by another person.

3. Accessing your MyCTOS report

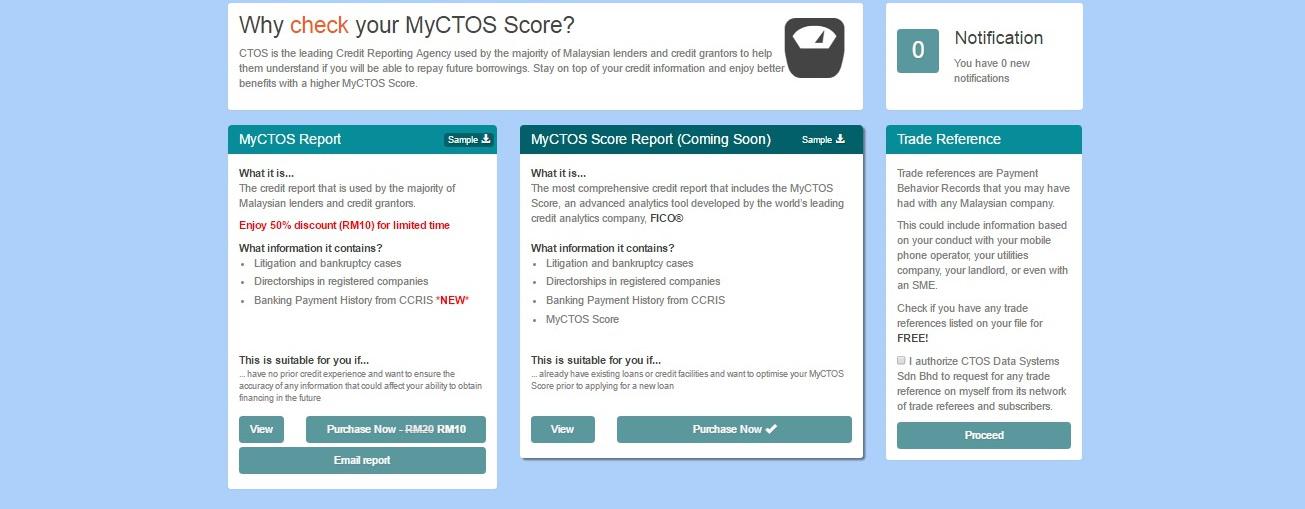

You will now have full access to view your CTOS report. Your first MyCTOS report is emailed to you for free, but you can also check it anytime you like on CTOS website.

Just login to CTOS using your login and password, and click on MyCTOS Report.

You will also get a special email account to use for CTOS purposes.

To add to your convenience of viewing your CTOS report, there is also a mobile app to let you view your report from your mobile.

What do financial institutions look at on your MyCTOS report?

The CTOS report mainly comprises identity verification, business exposure, directorships and business ownerships. It also contains details of legal actions, case statuses, bankruptcy information and your comments (wherever applicable).

The most important part of your report to a potential borrower is the third section, Financial History.

This section takes you down a memory lane of your financial history in 3 parts – recent credit application and CCRIS details, record of dishonoured cheques and your comment.

The CCRIS details is further broken down to 3 parts:

1. Outstanding credit

This section reveals your outstanding balance from existing credit facilities, including your repayment behaviour, arrears and legal status if any. Your repayment behaviour and arrears will tell if you are a good paymaster. If you have a number ‘1’ in your repayments, it shows that you are a month behind in your payments. If you are on time, it will be ‘0’ in the column of that particular loan. Legal status on the other hand, tells if you been sued by the existing creditor to pay up your dues.

2. Special attention account

All outstanding credit facility which are under close supervision by financial institutions will be under this column. This includes credit facilities that are deemed as Non-Performing Loan (NPL) or under special negotiated debt management schedules by Credit Counselling and Debt Management Agency (AKPK).

3. Credit application

This section will reveal if you have applied for any credit facility in the last 12 months, and if they have been approved or rejected. If your recent credit application had been rejected, it could mean that your credit-worth is questionable and extending a credit to you could mean you not being able to service its repayments. If it has been approved recently, then it is questionable why you require another credit facility and if you will be able to pay for it considering your existing commitments.

Under the comment column, you can explain why your financial behaviour has been as such. For example, you may have been unable to pay your dues because you lost your job and have no income.

Banks usually look at this section closely to determine if you are a good paymaster, and if you can still take on anymore credit based on your current credit facilities.

Unlike CCRIS where your records are kept only for 12 months, your CTOS records are kept for 24 months as a historical archive of your background and credit history. Thereafter, it will not be disclosed in your CTOS report two years after repayment or case settlement.

If you find there is a discrepancy in your CTOS records, you can request CTOS to modify or delete a certain information by providing the relevant supporting documents such as police reports, letters of support from relevant banks, lawyers or litigators or court order. CTOS will not charge you for updating your record and you will receive a free updated CTOS report thereafter.

There are many reasons why it’s important for you to check your credit report periodically, regardless of credit application. However, it is even more important if you are planning to apply for a credit, such as home loan or car loan.

You are doing yourself a disservice by applying for a loan without knowing what’s on your credit report because you are not giving yourself the best chance to get an approval. What if there is a credit card that you thought was cancelled but in fact has been charging your annual fees and interest for the past few years?

What if there is a discrepancy in the record of your payments or a bounced cheque that you have no idea of?

Checking your credit report is a proactive way of ensuring your credit health is good, and you are eligible for the credit you would like to apply for. A loan rejection can hurt your credit more than you think it does.